Features

AI Optimization

Transform Infinity Algo into a self-improving system that adapts to markets automatically.

Quick Setup

Enable AI

Turn ON

Enable AI Optimizationin settingsChoose Mode

- Backtesting? →

Static (Full History) - Live Trading? →

Walk-Forward

- Backtesting? →

Select Signal Type

Choose

AIorAI Sniperin Signal Mode

That’s it! Default settings work for most users.

How AI Works

| Simulate | Evaluate | Apply |

|---|---|---|

| Tests 100s-1000s of parameter combinations | Scores each using your metric | Implements best configuration |

Walk-Forward: Periodically re-optimizes on a rolling in-sample window and validates out-of-sample, reducing overfitting.

Core Settings

Optimization Modes

| Mode | How It Works | Use For |

|---|---|---|

| Walk-Forward | Updates every N bars | Live trading |

| Static | Optimizes once, locks | Backtesting |

Walk-Forward Only

100 bars (default) → Ultra-responsive (high CPU)

200-1000 bars → Balanced

1000-5000 bars → Very stable, slower to adapt

Examples on 1h chart:

- 100 bars = ~4 days

- 1000 bars = ~42 days

- 5000 bars = ~208 daysLower = More responsive but intensive | Higher = More stable and efficient

Parameter Space

| Range | Values | Best For |

|---|---|---|

| Very Fast | 5-9 | Scalping |

| Fast | 10-14 | Day Trading |

| Balanced | 10-20 | Most Strategies |

| Medium | 15-21 | Swing Trading |

| Slow | 22-28 | Position Trading |

| Auto | 5-28 | Full exploration |

Choose Your Goal

Quick Selection:

| Your Style | Use This Metric | Why |

|---|---|---|

| Scalping | Win Rate | Consistency matters |

| Day Trading | Sharpe Ratio | Balance risk/return |

| Swing | Sortino Ratio | Downside protection |

| Position | Calmar Ratio | Avoid drawdowns |

All Available Metrics:

- Classic: Total Profit, Win Rate, Average P&L, Gain-to-Pain

- Risk-Adjusted: Sharpe, Sortino, Calmar, Martin

- Advanced: SQN (System Quality Number), Robust ML Score

Simulation Settings

AI Sim TP% (Testing Only)

What they do:

- Help AI evaluate strategies

- Set internal profit targets

- Default: 1.0% both directions

Long TP: 1.0%

Short TP: 1.0%

Purpose: AI testing only

Real trades: Not affectedDashboard Display

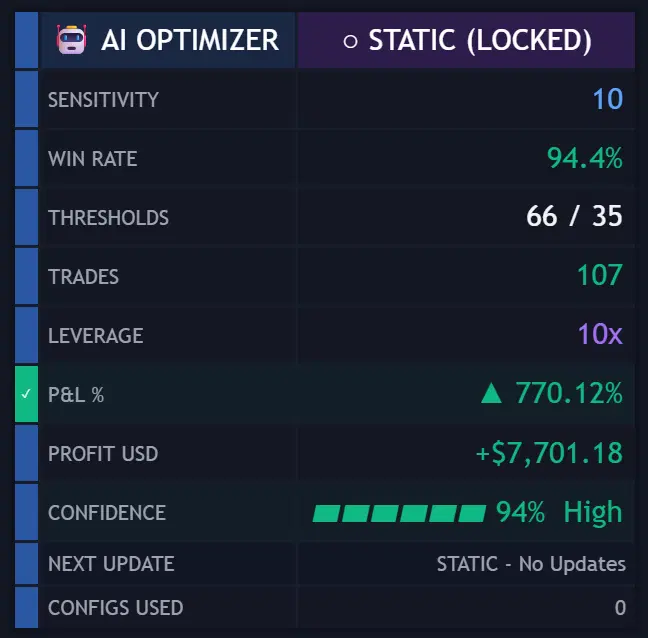

Live Monitoring

When enabled, see:

- Current optimal sensitivity

- Selected thresholds

- Win rate & metrics

- Confidence score

- Mode status

Status Indicators:

STATIC (LOCKED)— One-time optimization completeOPTIMIZING— Currently calculatingSIMULATED— Results ready

Best Practices

- Use Static for initial testing

- Select Balanced sensitivity

- Default 100 bar frequency

- Match metric to goals

- Walk-Forward needs ~535 bars for first optimization

- Static needs ~5000 bars total

- Lower timeframes → Complex calculations

- Monitor dashboard → Track selections

- Small adjustments → Better results

- Patience required → AI needs time

Limits:

- Max lookback: 5000 bars

- Lower frequency = Higher CPU

- Static = One calculation only at bar 4900

- Higher TF = Better performance

Troubleshooting

| Problem | Solution |

|---|---|

| Timeout | Use Static or increase frequency |

| No signals | Check AI Optimization is ON |

| Poor results | Try different metric/range |

| No dashboard | Enable in settings |

| Static fails | Need 5000+ bars data |

Quick Reference

For Testing

- Mode:

Static - Range:

Balanced - Metric:

Total Profit - Frequency: N/A

- Min bars: 5000

For Live Trading

- Mode:

Walk-Forward - Range:

Balanced - Metric: Your preference

- Frequency:

100(default) - Min bars: 535

Understanding Performance Metrics

Detailed Metric Explanations

Classic Metrics

| Metric | Formula | Best For |

|---|---|---|

| Total Profit | Sum of all P&L | Quick assessment |

| Win Rate | Wins ÷ Total trades × 100 | Consistency check |

| Average P&L | Total P&L ÷ Trades | Trade quality |

| Gain-to-Pain | Σ gains / |Σ losses| | Risk/reward balance |

Risk-Adjusted Metrics

Sharpe Ratio — Industry Standard

- Formula: Excess return (over risk-free) ÷ Standard deviation

- Infinity Algo: Uses risk-free = 0

- Pros: Most widely used, easy comparison, considers total volatility

- Cons: Penalizes upside volatility, assumes normal distribution

- Benchmarks: ~1 = Good | ~2 = Very good | 3+ = Outstanding

Sortino Ratio — Downside Focus

- Formula: Excess return (over target/MAR) ÷ Downside deviation

- Infinity Algo: Uses MAR = 0

- Pros: Only penalizes bad volatility, better for trend following

- Cons: Requires defining target return, less standardized

- Benchmarks: >1 = Good | >2 = Very good | >3 = Excellent

Calmar Ratio — Drawdown Protection

- Formula: CAGR ÷ Maximum drawdown (commonly 36 months)

- Pros: Focus on capital preservation, easy to understand

- Cons: Based on single worst event, backward-looking

- Benchmarks: >1 = Good | 3–5 = Strong

Martin Ratio — Ulcer Performance

- Formula: Excess return ÷ Ulcer Index (RMS of drawdowns)

- Pros: Considers all drawdowns, smooth equity curve focus

- Cons: Less known/comparable, complex calculation

- Use: Compare across your strategies

SQN — System Quality Number

- Formula: (Expectancy ÷ Std Dev) × √Number of trades

- Pros: Accounts for sample size, good for system comparison

- Cons: Requires sufficient trades for validity

- Benchmarks: >2 = Good | >3 = Excellent | >5 = Superb

Choosing by Trading Style

| Style | Primary Metrics | Secondary Metrics |

|---|---|---|

| Scalping | Win Rate + Sharpe | Total Profit |

| Day Trading | Sharpe + Win Rate | Average P&L |

| Swing Trading | Sortino + Calmar | Gain-to-Pain |

| Position Trading | Calmar + Martin | Sortino |